2026 Tax Guide: New Brackets, "Super" Catch-Ups, and Major Deduction Changes

Posted on December 30, 2025

Welcome to 2026! A new tax year is here, and with it comes a wave of inflation adjustments, fresh contribution limits, and some significant shifts in deductions that could reshape your financial planning.

Whether you are saving for retirement, managing an estate, or just trying to estimate your next tax bill, here is your essential guide to the 2026 tax landscape.

1. New Income Tax Brackets

The seven federal tax rates remain effective for 2026, but the income thresholds have shifted upward. This means you might earn more this year without jumping into a higher bracket.

For Single Filers:

- 10%: $0 – $12,400

- 12%: $12,401 – $50,400

- 22%: $50,401 – $105,700

- 24%: $105,701 – $201,775

- 32%: $201,776 – $256,225

- 35%: $256,226 – $640,600

- 37%: $640,601+

For Married Filing Jointly:

- 10%: $0 – $24,800

- 12%: $24,801 – $100,800

- 22%: $100,801 – $211,400

- 24%: $211,401 – $403,550

- 32%: $403,551 – $512,450

- 35%: $512,451 – $768,700

- 37%: $768,701+

2. Standard Deductions Are Up

The standard deduction has increased again, providing a larger buffer against taxable income for those who do not itemize.

- Single: $16,100

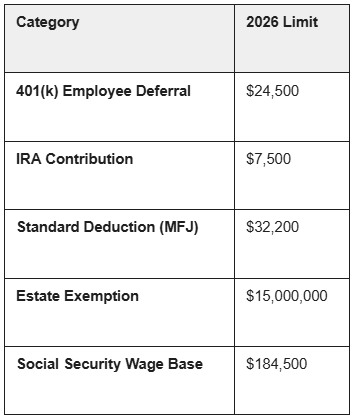

- Married Filing Jointly: $32,200

- Head of Household: $24,150

Note: If you are 65 or older, you can claim an additional deduction of $2,050 (Single) or $1,650 (Married).

3. Retirement Savings: The "Super Catch-Up" Is Here

2026 introduces distinct opportunities for late-career savers. While the standard limits have risen, a new "super" catch-up tier is now available specifically for those aged 60–63.

401(k), 403(b), and 457 Plans

- Standard Limit: $24,500

- Catch-Up (Age 50+): $8,000

- "Super" Catch-Up (Ages 60–63): $11,250

- Total potential contribution for ages 60–63: $35,750

IRAs (Traditional & Roth)

- Standard Limit: $7,500

- Catch-Up (Age 50+): $1,100

4. Notable Deduction Updates: The SALT Cap

One of the most eye-catching figures for 2026 is the adjustment to the State and Local Tax (SALT) deduction, which appears significantly higher than previous years.

- SALT Deduction Cap: $40,400

- Senior Deduction: A maximum of $6,000 is available, though it begins to phase out at $75,000 AGI for singles and $150,000 for couples.

- Qualified Overtime: A deduction of up to $12,500 is available for qualified overtime, subject to income phaseouts.

5. Estate, Gift, and Investment Taxes

For high-net-worth individuals, the exemption limits continue to climb, offering more room for tax-free wealth transfer.

- Estate Tax Exemption: $15,000,000 (with a 40% tax rate on excess)

- Annual Gift Tax Exclusion: $19,000 per recipient

- Capital Gains: The 0%, 15%, and 20% rates remain, with the 15% bracket now starting at $49,451 for singles and $98,901 for couples.

6. Social Security & Medicare

If you are a high earner or approaching retirement, keep these thresholds in mind:

- Social Security Wage Base: Tax applies to the first $184,500 of earnings.

- Earnings Test: If you claim benefits before full retirement age, $1 of benefits is withheld for every $2 earned above $24,480.

- Medicare Part B: Monthly premiums range from $202.90 to $689.90 depending on your income.

Let’s Start the Conversation!

Have questions or ready to plan your financial future? Fill out the form, and we’ll connect with you to provide expert guidance tailored to your needs!